Sunday April 7 marked the final day of the fifteenth edition of the International Multihull Show. At La Grande-Motte, on the shores of the Mediterranean, most of the shipyards’ sales managers were smiling from ear to ear. As they readily admitted, the show had been reassuring. Following a lukewarm Cannes Yachting Festival back in September, and a series of lackluster American boat shows - we won’t even mention boot Düsseldorf, boycotted by multihull builders in 2024 - it seemed legitimate to ask serious questions about market trends. At their early-season press conference, Groupe Bénéteau Managing Director Gianguido Girotti warned that “The years on cocaine are now over, and we’re back to normal!” The end of the Covid pandemic saw demand for multihulls explode. Many customers experienced a compelling desire to move ahead with a project that would have been still a long way off: they needed a multihull as soon as possible to be sure of being able to escape, be safe with their families, reconnect with nature... As a result, the pressure was transferred to suppliers, who began to experience inventory difficulties and consequently production delays. Delivery times were automatically extended. Inflation and geopolitical tensions quickly cooled the market’s extreme situation. For multihulls, the slowdown was less severe than in other sectors - but was nonetheless palpable having seen two decades of particularly strong growth.

An industry still with little automation

If we stick to the magic of the free, competitive market, are multihull prices set to fall after rising so spectacularly in recent years? If only the law of supply and demand applied, this would seem logical. But in reality, a multihull is an infinitely more complex asset than an intangible share on the stock market, whose price fluctuates every second. What’s more, building a catamaran or trimaran takes a relatively long time, and is still very much a manual operation, even if manu- facturing processes have been improved to save hours and protect the health of employees, notably with GRP parts now made by infusion. Nonetheless, labor still accounts for 60% of direct manufacturing costs for a mass-production multihull, compared with 40% for materials. For a 40-foot catamaran, no less than 1,200 man-hours are required. If you’re interested in a large custom multihull, you’re looking at tens of thousands of hours. We recently checked the production time for a 70-foot one-off: 30,000 hours had been clocked up! And that figure doesn’t include design and engineering time. In addition to the amount of labor required, hourly rates have also risen. Firstly, to keep pace with the inflation that employees have to contend with in their daily lives: for example, up 14.2% between 2019 and 2024 in France, the world leader in multihull manufacture. The marine industry as a whole employs a million people worldwide, including 42,000 in France (to which you can add 100,000 indirect jobs). According to France’s marine industries federation, the FIN, the domestic boating market generates sales of 4.95 billion euros. In comparison, the automobile sector generates sales of 101 billion euros (1,000 billion in the USA and 4,360 billion worldwide), with 218,000 employees. In France, sales per employee are therefore four times higher in the automotive sector than in the marine industry. What’s more, if we’ve taken the last five years as our benchmark, it’s because over this period we’ve added a second, sector-specific factor to the rise in salaries. The sharp rise in activity in the marine industry, particularly from summer 2020 onwards, has led to a real shortage of personnel, with over 1,500 vacancies to be filled each year. Competition between industries and between shipyards has therefore shifted to the recruitment arena, and companies have been forced to offer more attractive remuneration packages.

Raw materials, energy, insurance, rates... everything has gone up!

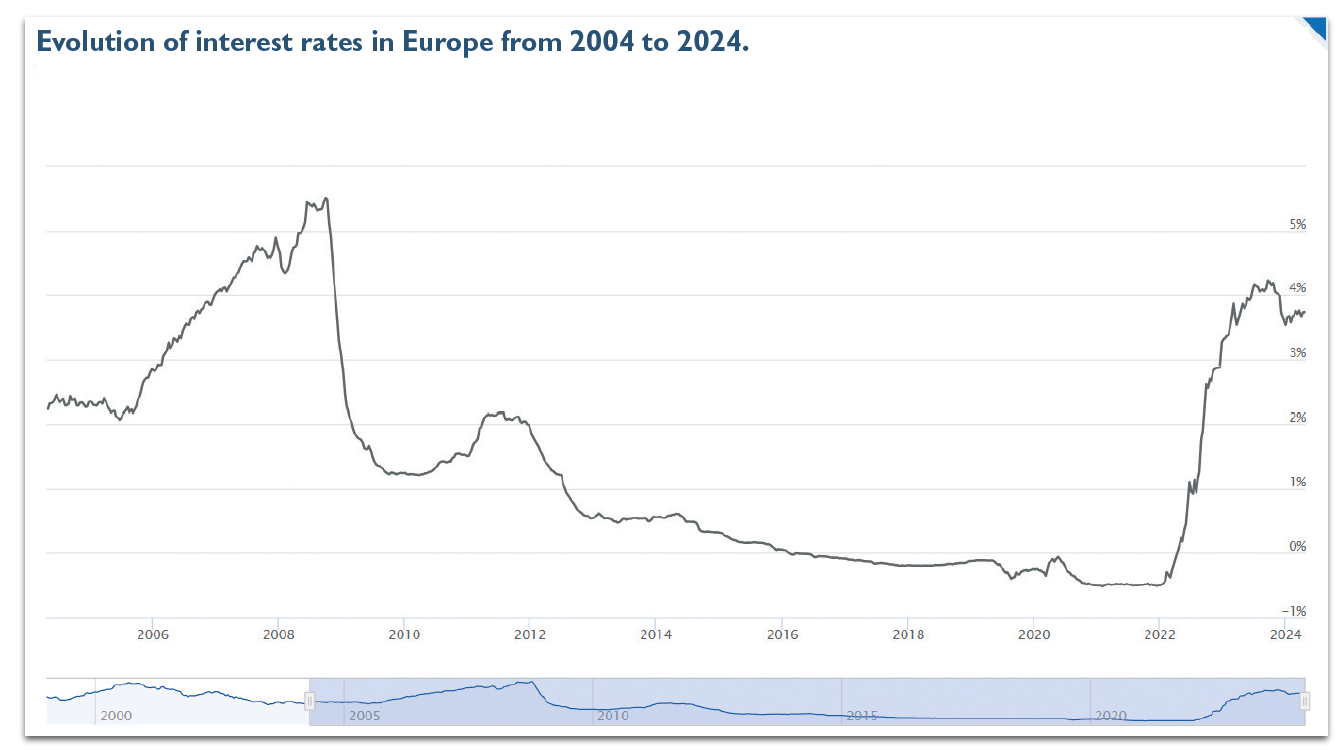

In terms of the raw materials from which most of our multihulls’ components are sourced, things have moved quite a bit too. The price of a barrel of crude oil, which stood at US$30 in 2004, has risen steadily - admittedly, it dipped momentarily to US$10 in April 2020, at the start of the Covid episode - until it reached US$122 in June 2022. It then stabilized at around US$80. Prices of aluminum (up 107.4%) and stainless steel (up 107.8%) more than doubled between 2020 and 2022. As a result, since 2014, the prices of our multihulls have started to rise - but not the margins! Yes, shipyard bosses are still flying economy class while their customers are one or two classes further forward... The published net results are certainly positive, and that’s the minimum in the buoyant environment of recent years, but we’re still within industry standards, i.e. between 5% and 8%. Only the Bénéteau Group has achieved double-digit earnings in 2023, with 10.2%. This is nothing like the margins seen in luxury goods, a world into which the marine industry is sometimes wrongly assimilated. Are we talking about the impact of interest rates or VAT/sales tax on Rolls Royce or Rolex? No, whereas in the yachting industry, two major events have influenced the market. After more than ten years of extremely low interest rates from 2010 to 2022 (see graph), their rise has increased the cost of credit financing. All the more so as, at the same time, Europe was putting an end to the tax niche that allowed you to benefit from a reduced VAT rate of 10% instead of 20% on the charter of boats purchased under what the French call a “Location avec Option d’Achat” (rental with purchase option) contract, more commonly known simply as leasing. This financing method was particularly advantageous for European residents. Since November 20, 2020, either you can prove that your multihull sails outside EU waters and then you don’t pay VAT on charters, or you pay 20% VAT. The only piece of good news for shipyards located mainly in the euro zone is that the European currency unit has been trading at an average of US$1.075 over the last three months, compared with US$1.20 three years ago, which is boosting exports. But between higher prices, higher interest rates and the loss of tax benefits, for a citizen of the European Union, the bill can be steep. We compared financing 6 years apart for a 40-foot catamaran of the same brand, with the same level of equipment, the same down payment (30%) and the same financing period (12 years): the monthly payments rose from € 2,618 in 2018 to € 4,275 in 2024, i.e. an increase of 63%!

A notable rise in prices

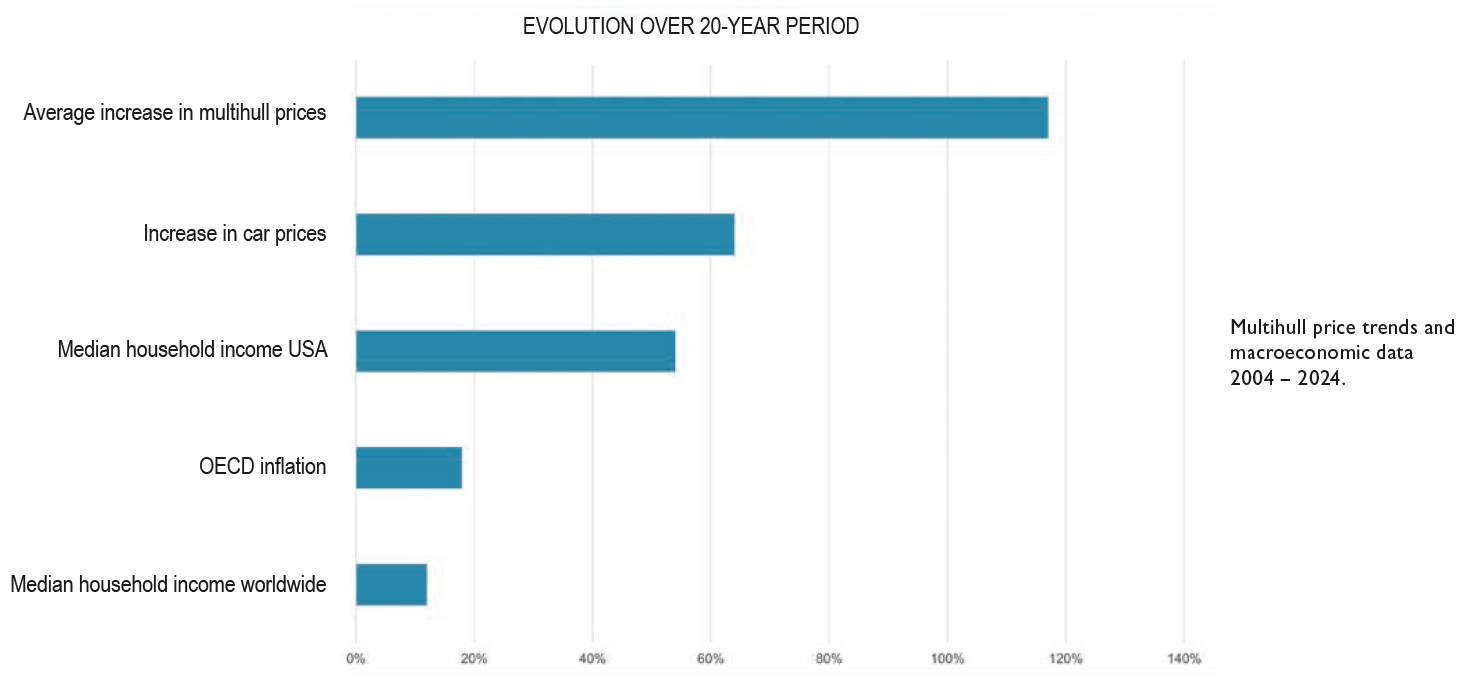

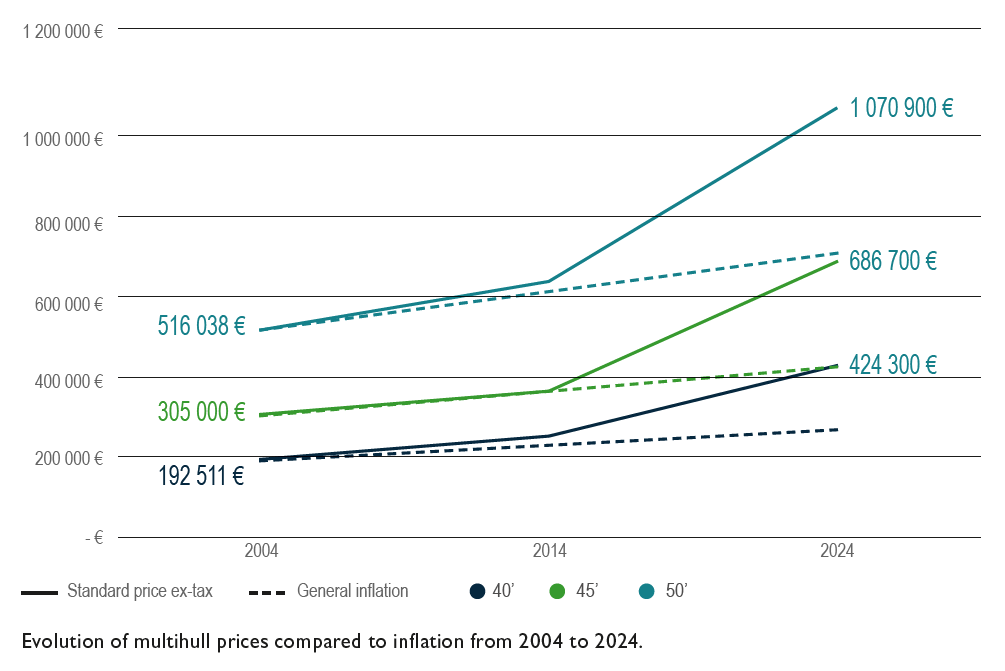

Looking at our graph, the acceleration in price rises is obvious over the last ten years. In fact, it’s especially since 2020 that things have accelerated. One manufacturer admits to having increased prices by 68% since 2018, another by 30% over the last two years, with similar orders of magnitude confirmed by other builders. Even for entry-level models, the rise is dizzying. Where twenty years ago you could buy a Lagoon 380 for € 226,393 excluding VAT (basic price), today you have to spend € 424,300 (87% more) to buy the Lagoon 40, both entry-level models of their time. We’ve taken this example because Lagoon, the world leader in its field, still has a fairly aggressive pricing policy, and all other shipyards have followed more or less the same trend. As can be seen from the attached graph, over the last 20 years, the average price of a catamaran, whether 40, 45 or 50 feet, has more than doubled. In France, cumulative inflation alone does not explain such a surge, since it represents 42.6% over this period; the Lagoon 400 “should” therefore cost just € 322,848. In the United States, taking into account cumulative inflation of 66.08%, the price would be € 375,993. We can see that the price increase is far higher than inflation in the countries where multihulls are sold...

It’s interesting to look at the automotive market for a comparison with the marine sector: let’s start with two examples, one on each side of the Atlantic. In the USA, the iconic Jeep Wrangler cost a minimum of US$ 16,270 in 2004; the base price is now set at US$ 33,890 - a 108% increase. In France, a Renault Clio 2 1.5 dCi previously cost €13,950; it now costs € 21,600 - an increase of 55%. If we generalize these observations, we can see that the average increase in car prices worldwide over 20 years is around 70%. This is significantly less than the increase in the price of our multihulls, but still higher than inflation in most “consumer” countries. And let’s not forget an important factor: during this period, purchasing power rose by around 10% in France and 30% in the United States.

4 (more or less good) reasons to raise prices

So why did multihull builders apply price increases 40-60% higher than inflation? There are four possible reasons. Firstly, like carmakers, manufacturers have clearly moved their models upmarket. Historic models that were so attractive twenty years ago, such as the Lagoon 380, the Athena 38, the Gérard Danson generation Outremer, the Aventura 36, the Leopard 40, or even the Nautitech 44 vintage 2004, would have a hard time finding takers today. Admittedly, on social media, the “things used to be better” brigade are pretty vocal, but for the most part only via their keyboards. Even on the second-hand market, these 20-year-old models are far less popular than their 5- to 10-year-old successors. The second reason for the rise in prices is quite simply, as mentioned above, the rise in raw materials and energy costs, as well as the price of many parts and equipment (motors, rigging, sails, etc.). The very long lead times also had an influence, combined with inflation: they forced builders to anticipate sharp price rises for the products mentioned above, sometimes for more than two years. The fourth factor is undoubtedly not the most glorious: most manufacturers, buoyed by their extremely full order books, simply decided to significantly increase their margins...

Price cuts, slower increases or opportunities?

But that was before! Average lead times have fallen back to around a year, or even a few months for certain models. There’s no point in dreaming: it will be very difficult, with very rare exceptions, to get your order delivered by the end of 2024... On the other hand, we’re entitled to ask THE question: will prices fall? Probably not, at least not in the short term. The only thing everyone seems to agree on is a pause in price increases (see reactions). However, a few “exceptional” offers are arriving in mailboxes, something that hasn’t happened for a long time in the multihull world. Yacht charter leader Dream Yacht Worldwide is offering a 2024 Lagoon 46 for sale, available immediately, in a charter management program of course. At Leopard Catamarans, pioneer and leader in power catamarans for cruising, you had to hurry to benefit from colossal discounts (27% to 29%) on the last powercats still available in 2024. The anticipated development of these models is dragging on a little, while the ranges are already well established, generating fierce competition and a de facto price war. In any case, discounts work for sailboats too: by the close of the International Multihull Show, Leopard was “sold out” on its three sailboat models (the 42, 45 and 50) for the year. It should be noted that Leopard sells direct, which facilitates the implementation of substantial discounts. For builders using dealer networks, the situation is more complex, as there is inevitably a time lag between market reality and dealer bookings. Especially since the latter, scalded by the supply difficulties caused by the post-Covid euphoria, wanted to protect themselves by booking a number of hulls that was perhaps a little optimistic in relation to the reality of the 2023-2024 season. At Istion Yachting in Greece, pre-orders are being taken for the summer of 2025. The next multihulls to be delivered will therefore be sailing as early as next winter - perfect timing to take advantage of the mild spring weather in the Aegean Sea. It takes a lot of perseverance to find the rare new multihulls available immediately, but it’s becoming possible. Naos Yachts in Los Angeles, for example, are offering a new Lagoon 40 and Lagoon 46. An opportunity totally unimaginable just a year ago. In the Fountaine Pajot network, it’s hard to find a catamaran available at short notice. “With the exception of an Elba 45 - 4 cabins cancelled by a major charterer, we’ll have to wait until 2025, even if we’re back on the right schedule for leaving the factory,” William Pauloin of Tendance Voile tells us.

The same goes for Canet Boat Plaisance, where you have to count on someone withdrawing or switching up to a bigger boat (when there was a three-year wait between order and delivery, it gave you time to change your mind!) to find an Elba 45 and even an Aura 51 available. Multihull Solutions in Australia, for its part, granted an exceptionally small price reduction on the excellent Neel 43, confirming that the slowdown is more noticeable in the “smaller” sizes than in the larger units.

So, yes, there’s a visible lull in the market, but no major upheaval to be expected in the short term, and no speculative bubble bursting in sight. Rather, industry professionals are talking about a “return to normal”, which is good news for potential buyers. Delivery times are now reasonable, relations with sellers are more balanced, and it’s no longer forbidden to dream of a good opportunity... Witness the new Lagoon 43, advertised at the same price as its predecessor, the 42 - a model which is also available in over-equipped, end-of-series mode at a very attractive price.

Thibaut de Montvalon Brand Director, Excess Catamaran

“The International Multihull Show proved to be a pleasant surprise for us, as sales were better than in 2023. Nevertheless, such a show remains a bit of a blip within a general environment that is undeniably calmer. There is perhaps a little too much supply (new and pre-owned) for demand. And private owners and charter companies are investing less these days.

There are many brands, many models, and many shipyards have increased their production capacity... an adjustment will take place over the next 12- 18 months, that’s for sure. We continue to attract new customers, who are not shocked by prices - but these buyers are all the more demanding in terms of quality, service and support. We’re also benefiting from the novelty effect and the trend towards outdoor leisure activities since Covid, particularly for a whole generation of 40–60-year-olds, who are “young at heart”, or young in their heads!”

Matthieu Rougevin-Baville Sales Director, Outremer Yachting

“The International Multihull Show turned out to be as positive and international as ever for us: at the 2024 edition, we welcomed as many prospects as last year and signed just as many catamarans. Paradoxically, shorter delivery times are enabling us to win more sales, because buyers find it hard to project themselves into a situation three years on. We don’t expect any price increases in 2024, despite declining profitability ratios due to rising costs of energy, insurance, transport and labor. With the acquisition of the Marsaudon Composites yard in Brittany and a better, more efficient layout of the La Grande-Motte site, here in the South of France, we can even envisage increasing our annual production capacity by around 25%.”

Boris Compagnon Sales Director, Catana Group

“The IMS was somewhat lowkey for us. There was no euphoria, but the buyers were there all the same. We have a little less visibility on the order book, meaning we’re therefore more cautious and ready to adapt our production capacity. On the other hand, we’re not planning any price cuts on existing models. That choice is all the more justified in that we are celebrating Bali’s tenth anniversary, and all our distributors are offering an anniversary package to mark the occasion. All the same, I’m noticing that the new models we’re introducing, as well as those from our competitors, are coming in at more reasonable prices than two years ago.”

Brieuc Maisonneuve Sales Director, Neel Trimarans

“La Grande-Motte was a fairly good show, with more sales than in 2023, although we hadn’t necessarily expected this. But over 12 months, demand for the smaller models remains weak. The brand continues to be driven by its best-seller, the Neel 52, for which customers now have to wait until the second half of 2026 for delivery. Because of its youth and strong, rapid growth, the company is lagging a little behind inflation and the increases achieved by other yards. So, inevitably, we’ve lost a little in terms of profitability, but for the same reasons, there are major sources of productivity. Everyone in-house is working hard to reduce production times and cut costs. We continue to offer simple, seaworthy trimarans, with the comfort of our catamaran brethren, but more personalized and better finished than we have been able to do in the past. We were also delighted to deliver a Neel 47 to Yannick Bestaven, the reigning Vendée Globe winner, and to organize our Private Days event on June 14, 15 and 16, where we were able to invite all interested parties to come and try out our trimarans.”